Simulation, Optimization, and Machine Learning for Finance (Second Edition)

Introduction to the Book

The second edition of Simulation, Optimization, and Machine Learning for Finance by Dessislava Pachamanova, Frank J. Fabozzi, and Francesco Fabozzi represents a significant step forward in the way quantitative methods are applied to finance. The book addresses the transformation of financial markets, where computational tools, large datasets, and artificial intelligence are now indispensable for investment, risk management, and corporate decision-making. Unlike conventional finance textbooks that focus on single methods, this book integrates three powerful approaches—simulation, optimization, and machine learning—into a unified framework, demonstrating how they complement each other to solve real-world financial problems.

Simulation in Finance

Simulation is one of the central tools in modern financial analysis because markets operate under uncertainty. Traditional models, such as the Black-Scholes formula, assume simplifications like constant volatility or log-normal asset price distribution. However, real markets often violate these assumptions. Simulation allows analysts to model complex scenarios by generating artificial data based on stochastic processes.

For example, Monte Carlo simulation can project thousands of possible future paths for asset prices, interest rates, or credit spreads. This provides not only expected returns but also the distribution of risks, tail events, and probabilities of extreme losses. In risk management, simulation underpins stress testing, value-at-risk (VaR) analysis, and scenario generation for portfolio resilience. In corporate finance, it plays a role in evaluating projects with embedded flexibility through real options. Thus, simulation provides the foundation for understanding uncertainty before applying optimization or predictive modeling.

Optimization in Finance

While simulation generates possible outcomes, optimization determines the “best” decision given constraints and objectives. In finance, optimization problems often involve maximizing returns while minimizing risk, subject to real-world limitations such as transaction costs, regulatory requirements, and liquidity considerations.

The classical example is Markowitz’s mean-variance optimization, where portfolios are constructed to achieve the maximum expected return for a given level of risk. However, real portfolios face nonlinear constraints, higher-order risk measures (like Conditional Value at Risk), and multi-period rebalancing challenges. Optimization methods such as linear programming, quadratic programming, and dynamic programming extend beyond the classical models to handle these complexities.

Optimization is not only for portfolios—it applies to corporate capital budgeting, hedging strategies, fixed-income immunization, and asset-liability management. In modern finance, optimization must integrate outputs from simulations and predictions from machine learning models, creating a loop where all three methods interact dynamically.

Machine Learning in Finance

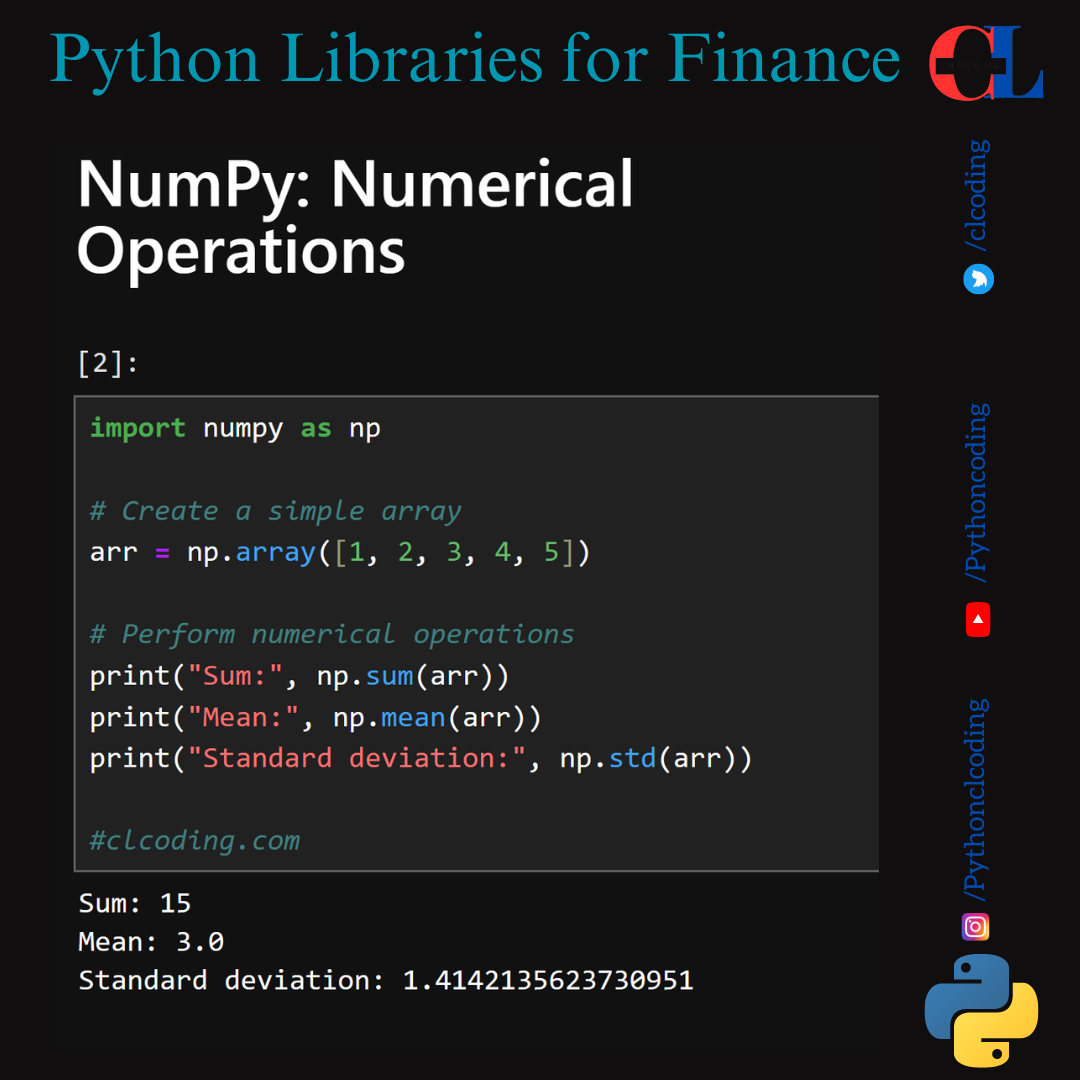

Machine learning has shifted from being an experimental tool to a mainstream component of financial decision-making. Unlike traditional statistical models, machine learning techniques can handle high-dimensional data, nonlinear relationships, and complex patterns hidden in massive datasets.

In finance, supervised learning algorithms (such as regression trees, random forests, gradient boosting, and neural networks) are applied to forecast asset prices, detect fraud, and predict credit defaults. Unsupervised learning techniques like clustering help identify hidden market regimes, customer segments, or anomalies in trading data. Reinforcement learning has begun influencing algorithmic trading, where agents learn to maximize cumulative profit through trial and error in dynamic markets.

Importantly, the book does not present machine learning in isolation. It connects ML to simulation and optimization—showing, for instance, how ML can improve scenario generation, refine predictive signals for portfolio optimization, or enhance stress testing by identifying nonlinear risk exposures.

Integration of Methods: The Unified Framework

The true strength of this book lies in demonstrating how simulation, optimization, and machine learning are not separate silos but interconnected tools. Simulation provides realistic scenarios, optimization chooses the best decisions under those scenarios, and machine learning extracts predictive patterns to improve both simulation inputs and optimization outcomes.

For example, in portfolio management, machine learning may identify predictive factors from large datasets. These factors feed into simulations to model uncertainty under different market conditions. Optimization then uses these scenarios to allocate capital most effectively while controlling for downside risk. Similarly, in corporate finance, machine learning can forecast demand or price volatility, simulations model possible business outcomes, and optimization selects the best investment strategy given uncertain payoffs.

This integration reflects the modern reality of financial practice, where decisions must account for uncertainty, constraints, and ever-growing data complexity.

Applications Across Finance

The book goes beyond theory by covering a wide spectrum of applications:

Portfolio Management: Extending classical models with advanced optimization and machine learning signals.

Risk Management: Stress testing, Value at Risk (VaR), Expected Shortfall, and tail-risk measures supported by simulation.

Fixed Income Management: Duration-matching, immunization, and stochastic interest rate modeling.

Factor Models: Building robust multi-factor models that integrate machine learning for improved explanatory power.

Real Options & Capital Budgeting: Using simulations to value managerial flexibility in uncertain projects.

This breadth ensures that the book remains relevant not only for asset managers but also for corporate strategists, regulators, and risk professionals.

Challenges and Considerations

Although powerful, these tools are not without limitations. Simulation results are only as good as the assumptions and input distributions used. Optimization models can become unstable with small changes in inputs, especially when constraints are tight. Machine learning models, while flexible, risk overfitting and lack interpretability. The book acknowledges these challenges and emphasizes the importance of combining theory with sound judgment, validation, and computational rigor.

Hard Copy: Simulation, Optimization, and Machine Learning for Finance, second edition

Kindle: Simulation, Optimization, and Machine Learning for Finance, second edition

Conclusion

Simulation, Optimization, and Machine Learning for Finance (Second Edition) is more than a textbook—it is a roadmap for navigating modern financial decision-making. By weaving together probability, simulation, optimization, and machine learning, it equips students, researchers, and practitioners with the tools needed to manage uncertainty, exploit data, and make rational decisions in complex financial environments. Its emphasis on integration rather than isolation of methods mirrors the reality of today’s markets, where success depends on multidisciplinary approaches.

.png)

.png)